What the DoW’s Accelerated Research for Transition (ART) Program Actually has to Prove

The Valley of Death has had many bridges. ART is another.

Congress passed the Small Business Innovation Security Act on 14 April this year. The DoW passed the Accelerated Research for Transition (ART) six days later. Over 90 SBIR/ STTR topics opened less than a week later. The press hailed the answer to the valley of death. Founders and capital allocators treated ART’s approval as a next-to-IPO grade signal.

Let’s pause here. The framing around ART has run ahead of the evidence we already have. “The valley of death” is becoming a lazy cliche. The federal government has already built bridges across it: RIF, STRATFI, TACFI, CATALYST, APFIT, OSC, and Strategic Breakthrough awards. These all debuted with similar rhetoric-- some worked and some didn’t. ART is neither the first attempt of its kind nor guaranteed to do better than any of its predecessors.

What ART is

Let me clearly define what ART is, first. To understand ART, we have to understand the government’s Small Business Innovation Research (SBIR) and Small Business Technology Transfer (STTR) programs. They’re essentially seed funding from the federal government: non-dilutive, early stage R&D funding for small businesses to encourage technological innovation with public benefits. There was a ~6 month lapse in SBIR/ STTR funding before the Small Business Innovation and Economic Security Act reauthorized SBIR/ STTR funding through FY2031.

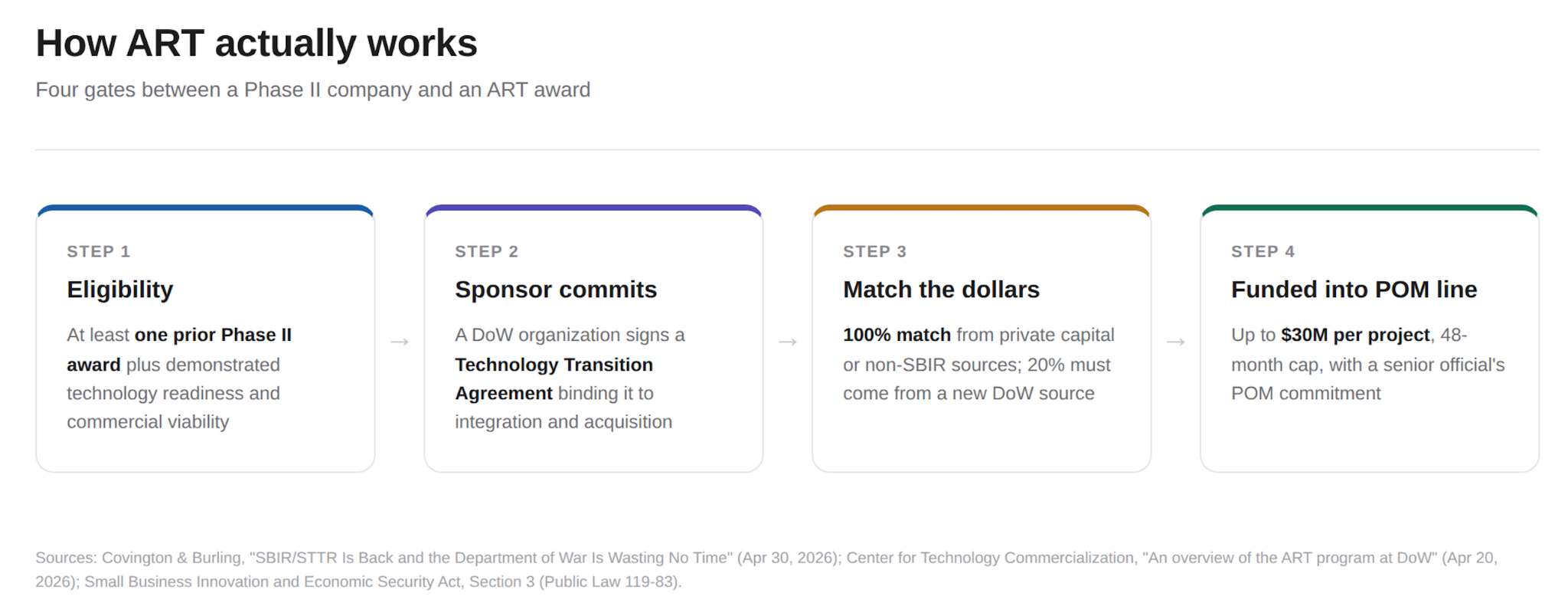

For simplicity’s sake, it is incredibly difficult to move from SBIR/ STTR funding to full procurement (more on that here). So, the DoW introduced ART on 20 April to help transition phase II SBIR/ STTR programs into phase III outcomes-- in other words: to help SBIR/ STTR awardees cross the infamous valley of death.

ART functions by providing a 1:1 match between DoW dollars and ART funds to new or existing phase II contracts. The sponsoring organization within the DoW must agree to a Technology Transition Agreement that commits the sponsoring organization to integration and acquisition of the technology it sponsors. Tangibly, ART provides: up to $30mm in funding per project, a 48-month performance cap, and a 100% match from new private capital or government funding sources outside of SBIR.

To be clear: this new funding mechanism provides more rigor than the legacy SBIR system. The question isn’t whether ART is good or bad. The question is: do ART’s features address SBIR’s selection problem?

The selection problem problem ART inherits

Let’s honestly recount SBIR’s record.

Let’s start with the good. Josh Lerner published a foundational 1998-99 study that finds SBIR awardees grow significantly faster than matched companies over a decade. This effect amplifies in zip codes with significant venture capital activity. Qualcomm received $1.1mm in early SBIR awards along with ViaSat, goTenna, AeroVironment, and Vita Inclinata. Anduril’s $12mm turned into hundreds of millions in Phase III.

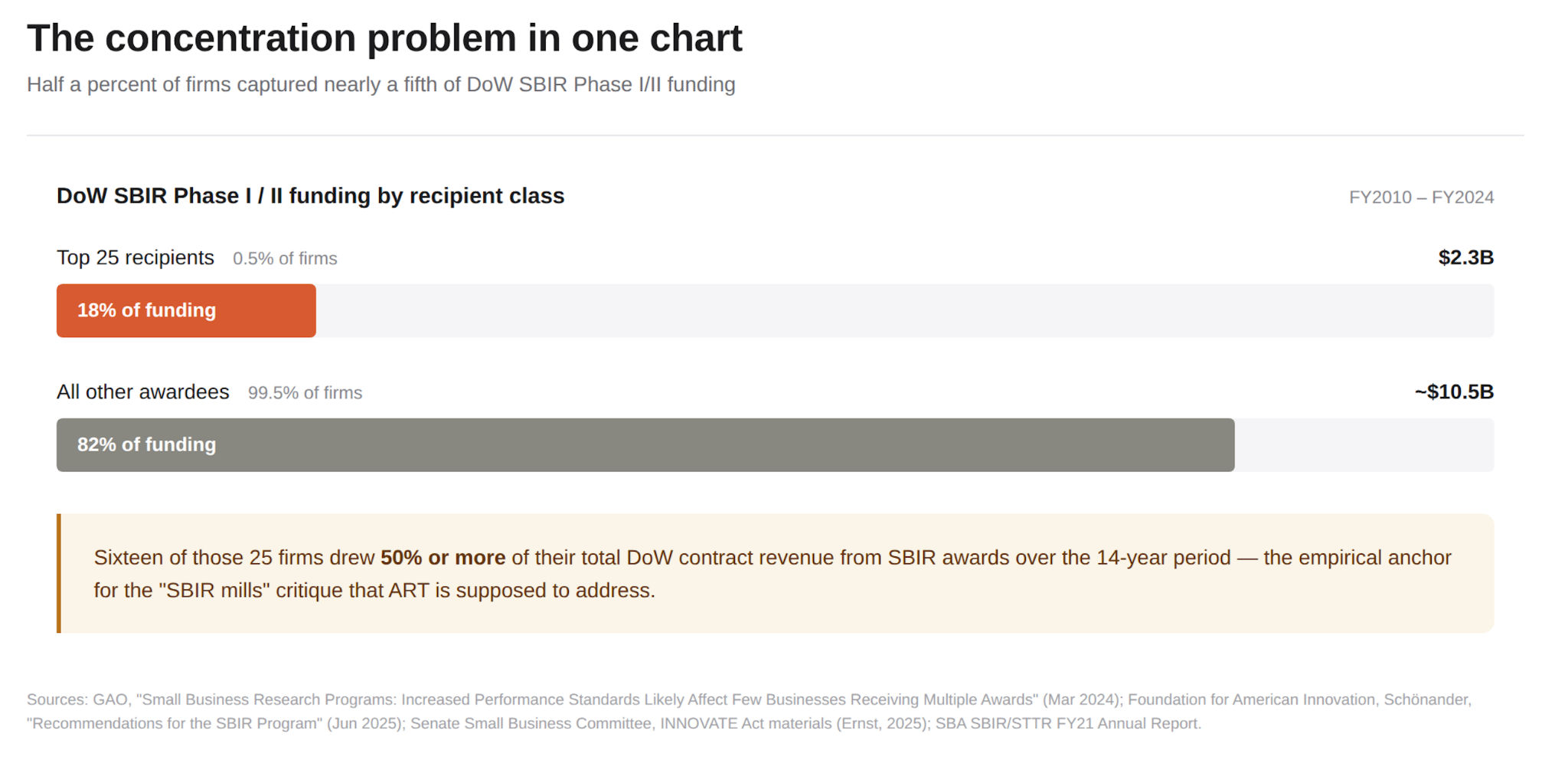

Here, however, is where SBIR doesn’t work: SBIR mills. These firms frequently win countless SBIR grants but use the program as their primary revenue stream; not to commercialize their research. 25 companies received 18% of all DoD SBIR Phase I/II funding over a decade. That’s $2.3b concentrated in 0.5% of participants. The Defense Innovation Board found 61% of SBIR Phase III transitions generated more in Phase I and II funding than in Phase III contract revenue, and sixteen of the top 25 SBIR recipients drew over 50% of their revenues from SBIR awards over 14 years.

Of course, there’s a give and take between these dueling conceptions of SBIR’s merits. Robert Atkinson of CSIS argues funding in frontier technologies like quantum concentrates out of necessity. Of course, the truth lies somewhere between these competing narratives. SBIR-- in its 40 year history-- has proven itself as both a legitimate funding source for real innovators and a mere subsidy for firms who do nothing but apply for and win awards. ART’s key to success is to what extent it allocates money to the real innovators; that hinges on SBIR’s ability to select the right ideas rather than transition them into programs of record.

The record on bridging the Valley of Death

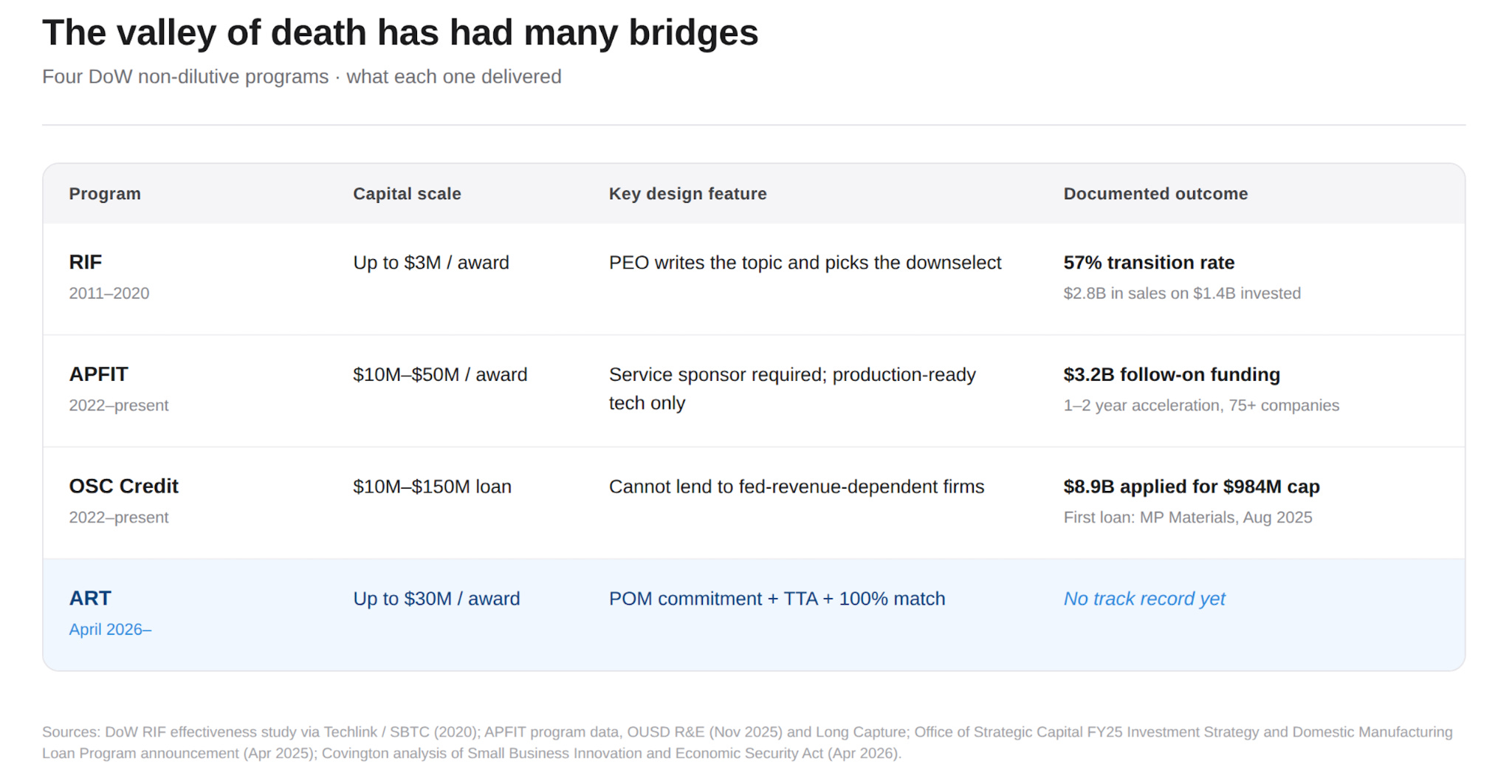

Rapid Innovation Fund (RIF) | 2011-2020

The 2011 National Defense Authorization Act (NDAA) created RIF-- essentially, this was procurement money for SBIR Phase II winners. The DoW’s own assessment of RIF’s success reported 670 awards that summed to $1.4b, a 57% transition to fielding rate, and $2.8b in resulting sales, and the Navy reported 40% of its RIF technologies were fielded within five years. RIF worked. Then COVID happened. The fact that even programs that worked got killed is important to keep in mind here.

Accelerate the Procurement and Fielding of Innovative Technologies (APFIT) | 2022-present

APFIT is procurement funding for ready-to-produce technology with a service sponsor that provides a 1-2 year track to program of record status instead of the traditional acquisition path. APFIT’s track record: $1.4b awarded to over 75 companies with $3.2b in follow-on funding. APFIT has worked for three reasons relevant to ART. 1.) APFIT is procurement money. Companies must have a ready-to-field product. 2.) APFIT requires a service sponsor like the Army or Air Force that maps to a real program, and 3.) it selects on demand (or lack thereof) from a service.

Office of Strategic Capital (OSC) | 2022-present

OSC is effectively a loan provider. OSC’s inaugural notice of funding availability (NOFA) garnered over 200 applications that summed to $8.9b in requests for $984m in unallocated capital. OSC’s genuine innovation lies in the fact that it can’t lend to companies whose repayment is mostly dependent on federal sources. That means SBIR mills can’t qualify for OSC loans. OSC inherently selects companies with pre-existing commercial market viability.

Strategic Funding Increase (STRATFI); AFWERX | 2019-present; 2017-present, respectively

These are larger SBIR Phase II awards that combine SBIR dollars, non-SBIR government dollars, and private capital. STRATFIs need SBA waivers for going over the $60mm threshold, but even at this size, “$60mm will not productize many technologies needed by the DoD.”

The pattern

Three commonalities emerge from the capital bridges that work:

Requiring downstream commitment from someone outside of SBIR

Sizing to the actual capital intensity of moving from prototype to product

Creating selection pressure that excludes SBIR mills

So, how does ART compare?

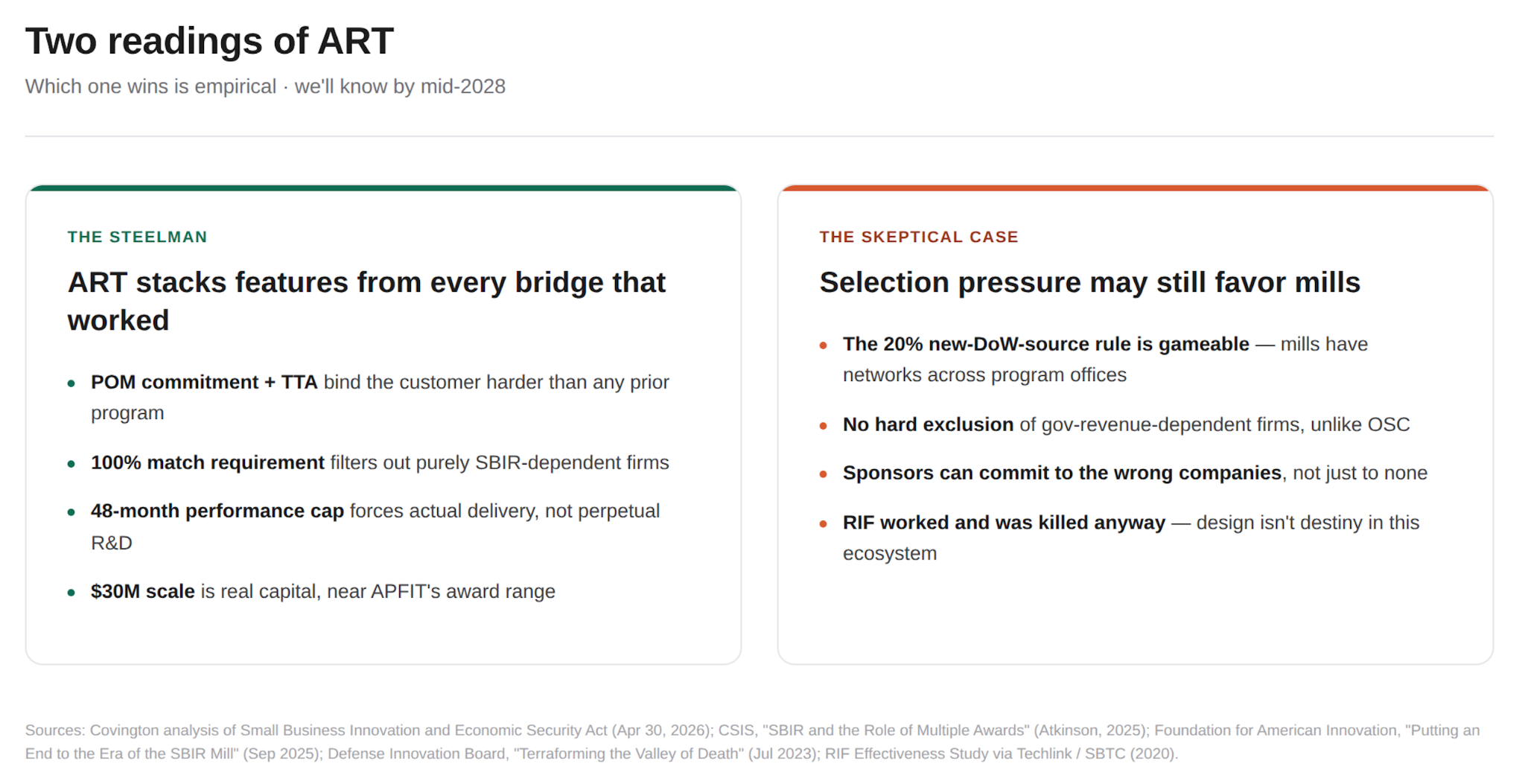

ART certainly boasts a downstream commitment feature: both the Technology Transition Agreement and Program Objective Memorandum POM commitment provide real rigor. However, ART lacks a hard exclusion of firms with government-dependent business models. ART also lacks any requirements that companies be production-ready and not just prototype-ready.

This is where the current framing gets ahead of available evidence. Many are celebrating ART as the bridge over the valley of death that will finally work. Yet the bridges that have largely worked boast features ART partially adopts. ART might work for SBIR winners with credible commercial paths. However, ART probably won’t work for multi-decade SBIR shops, and there’s nothing in ART’s design that makes it harder for those companies to qualify for ART funding.

Of course, the requirement for a 20% match from new DoW sources is the most compelling case for ART being a step in the right direction. It pushes companies to bring in new customers in the DoW. I, however, question how that translates from theory to practice. There are businesses that have been figuring out how to satisfy requirements like this for 40 years. SBIR mills no doubt have networks in multiple program offices. 20% from a new DoW source is real, but it may not be structural enough to disrupt the status quo in which SBIR shops sit.

The case for ART

There is also the possibility that SBIR’s transition problem is a structural problem; not a selection problem. Phase II awards end, companies have working tech, but no one in the DoW has the authority or money to buy it, so the company runs out of money and dies. ART solves this problem binding sponsor money and ART money together under a Technology Transition Agreement that requires the senior acquisition official to commit to a program objective memorandum (POM) line to the company. That’s real commitment; POM lines are how the DoW actually buys stuff.

Moreover, the Strategic Breakthrough authority within ART has a legitimate mandate, as $30mm can make a real difference in transitioning SBIR winners. The 48 month performance cap forces real delivery by the funding recipient, and eligibility requirements-- prior phase II funding, demonstrated commercial viability, and a 100% match-- filter out mere concept companies.

ART also provides a possible pseudo network effect. The Foundation for American Innovation argues opening Phase 1A and selection process reform will dilute SBIR mill influence. Even partial success for ART creates an alternative path that attracts sharper applicants and reshapes the applicant pool over time. Most relevantly, ART could be the first DoW program that combines RIF’s downstream commitment design with OSC’s matching structure and APFIT’s POM-line mandate. These features combined with the DoW’s recent organizational restructuring create a coherent case for this time genuinely being different.

As I see it, the key piece for ART to win is a significant number of companies that deliver products into POM lines in 48 months. This first cohort’s transition rate will tell us whether ART’s design selects (or fails to select) for the right companies. Keep an eye on who applies, who has prior commercial revenue, how many are first time SBIR participants, and whether the 20% new source rule seems to meaningfully filter the applicant pool.

ART in context

Okay, enough with the ivory tower navel gazing. What does this really mean for defense tech?

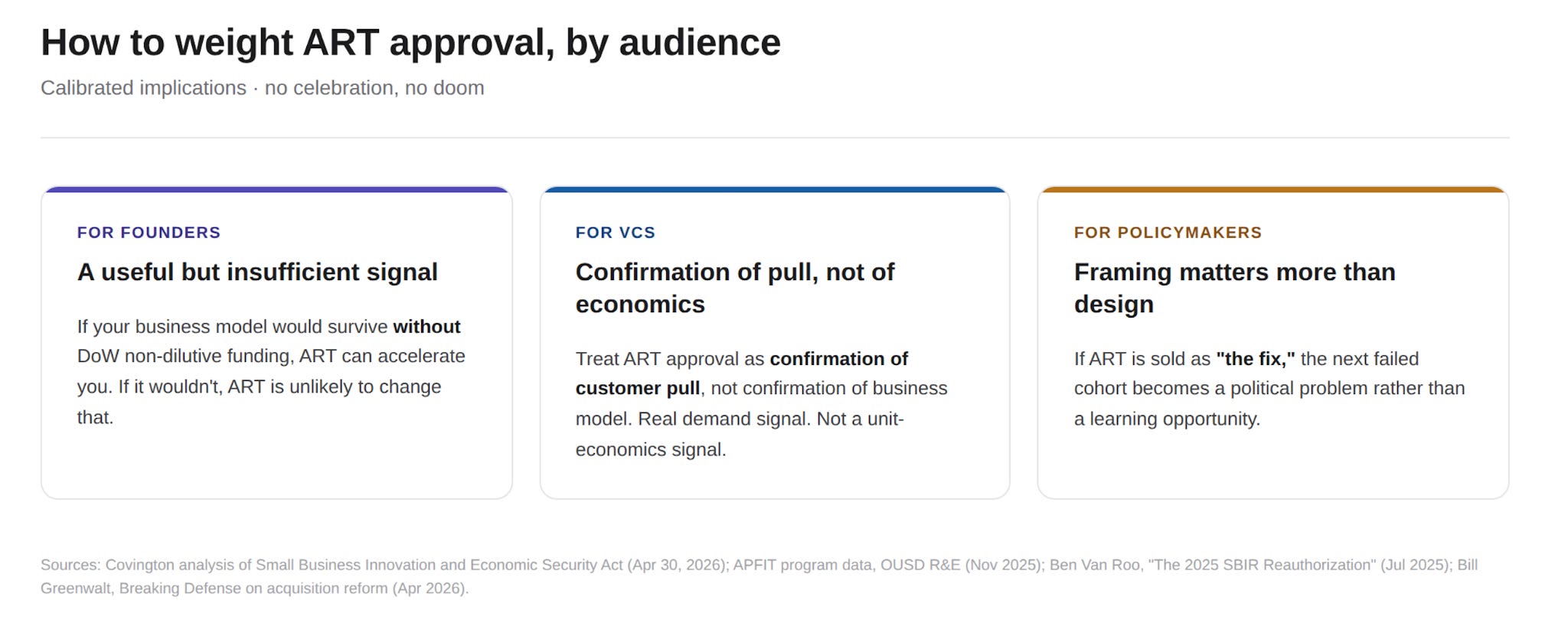

For founders

ART approval’s a useful signal but nothing more than that. Don’t build your business plan around it. Valley of death escapees like Shield AI and Saronic utilized SBIR as a complement to venture funding rather than a primary growth path. ART’s selection rule is generally: if your business would survive without DoW funding, ART can help you move faster. If not, ART won’t change that.

For capital allocators

Account for ART approval, but don’t overindex on it. DoW funding bridges that worked before produced winners that would have been winners irrespective of DoW funding. ART will tell you more about a founding team’s DoW GTM expertise and what capabilities the DoW wants. ART is-- more than anything-- an indicator of customer appetite for a product.

For policymakers

Framing matters here. Selling ART as a silver bullet makes the next failed cohort a political problem instead of a learning opportunity. A more measured framing clarifies that ART is an attempt to solve a problem that has been resistant to multiple prior attempts to solve that problem.

The pattern in who crosses the valley of death hinges on whether or not a company possesses a business model that doesn’t need non-dilutive funding to survive. ART helps those companies go faster. Let me offer a clear, falsifiable hypothesis here: ART’s design didn’t fix the selection problem if the first ART cohort transition rate to POM lines is below 40% within 24 months.

By then, we’ll know whether ART’s first cohort delivered into POM lines, whether the 20% new source rule actually moved the needle on selection, and whether the DoW developed the discipline to kill underperforming projects. Until then, however, cautious optimism is the appropriate posture. The valley of death has had plenty of bridges. ART is merely a new one.